As banking in Africa proliferates and becomes increasingly digital, financial institutions are left grappling with two key challenges on their journey to growth:

- How to accelerate customer acquisition?

Implement an onboarding process that is fast and frictionless, and complies with industry regulations. - How to reduce and counter the risk of identity fraud?

Ensure our customers and our assets are safeguarded against fraudulent activity and penalties.

To effectively control and manage the risk from identity fraud the customer onboarding process should be able to reliably verify that people are who they say they are. This prevents fraudsters from entering banking systems and creates a barrier at the first checkpoint.

Contents:- Your first interaction with customers can make or break their experience

- Digital self-onboarding - fast, frictionless and secure

- Benefits of digital self-onboarding for financial institutions

- How digital self-onboarding reduces the risk of identity fraud

- Laboremus is leading the change towards digital banking in Africa

Your first interaction with customers can make or break their experience

Global research shows that a staggering 9 out of 10 businesses experience some form of attrition during the onboarding process, with the banking sector experiencing the highest rate of drop-outs at almost one out of every four new customers.

Customers cite long and complex onboarding flow as a primary reason for abandoning their onboarding experience midway. This is a massive a loss of business revenue and also damages the company’s reputation in the market.

The future of banking in Africa is digital. Your customers today demand a purely online, 24x7 access to financial services and products.

For banks and other financial institutions a comprehensive, fast and convenient digital experience becomes critical in attracting new customers and retaining them over a long period of time.

And of course, the memorable customer experience begins with the customer onboarding process which is the first interaction your customers have with your brand.

Digital self-onboarding - fast, frictionless and secure

With digital self-onboarding companies acquire new customers by having them enter information digitally directly into their online user platform. The onboarding can be setup on your website, in-app and, crucially, in branch-assisted or agency-assisted environments.

In all cases, digital customer onboarding platform performs the necessary due diligence on every customer application, with relevant know your customer (KYC), know your business (KYB) and AML-PEP requirements. With self-onboarding it is vital to establish security procedures to ensure people are who they say they are. This is done via identity verification, digital footprint analysis, and through customers due diligence.

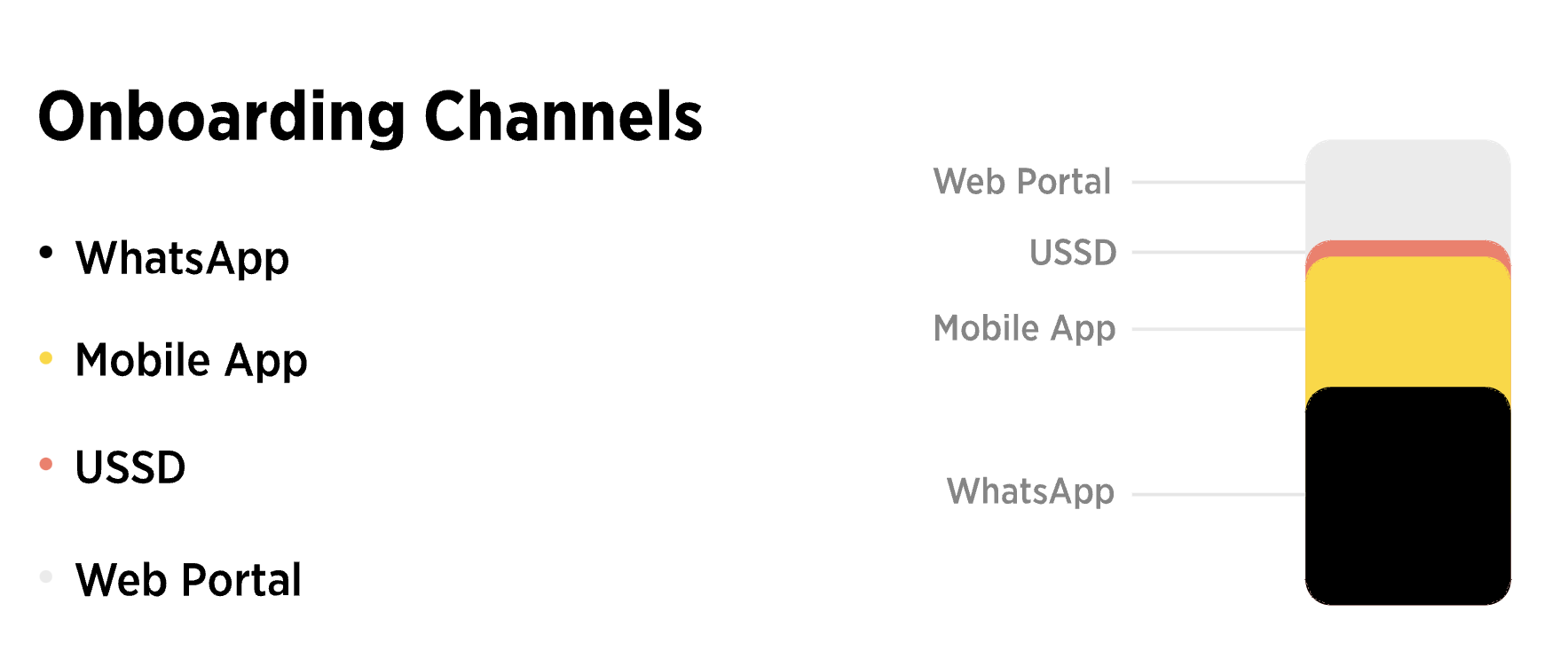

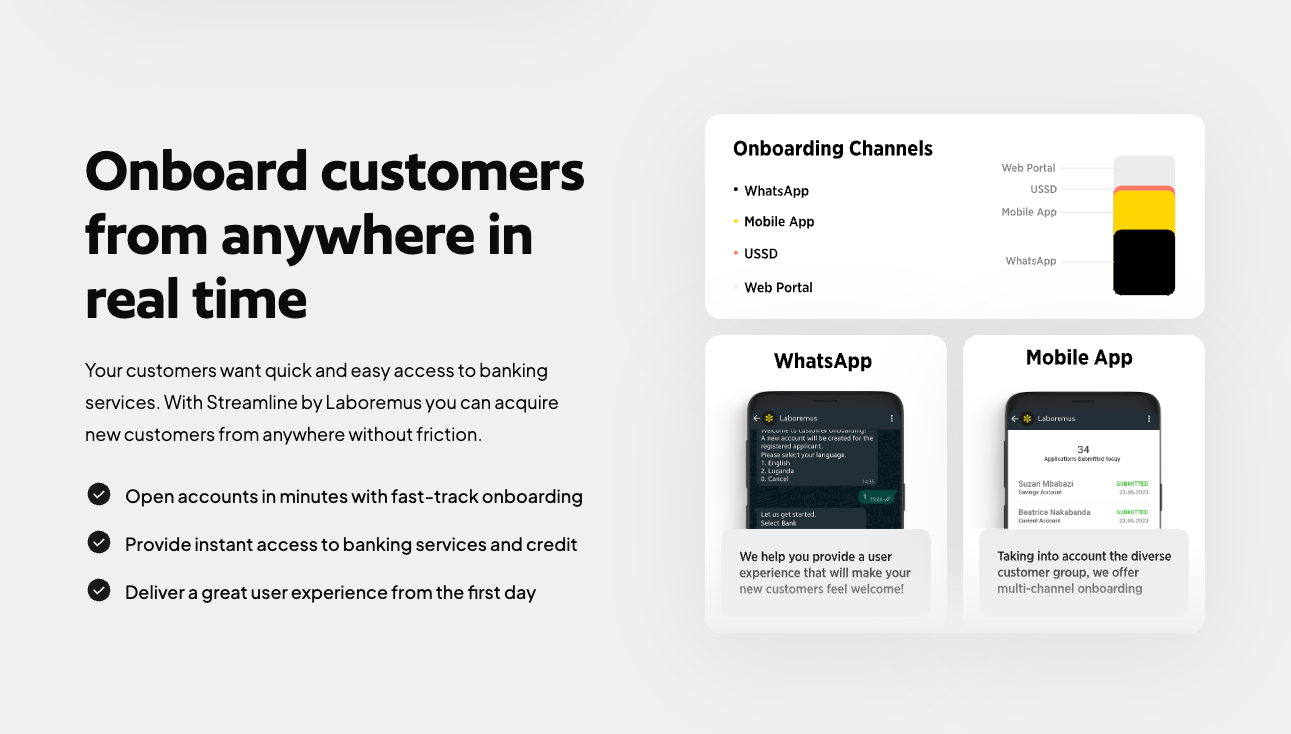

In Africa, Laboremus is driving adoption of digital self-onboarding for financial institutions across 4 key channels:

- USSD

USSD digital onboardingempowers customers to open a bank account using their mobile phones through USSD codes. The codes are sent over cellular networks and don’t require internet connectivity for communication. USSD digital onboarding is designed to make banking more accessible, particularly in areas with limited access to traditional banking services.

- WhatsApp

WhatsApp is a secure and convenient channel for providing banking services, and it allows customers to interact with their bank in a familiar messaging app environment using automation and chatbots. WhatsApp allows the designing of more sophisticated onboarding process as customers can upload pictures and important documents necessary to complete the digital KYC prior to account opening.

- Web browser - Mobile and Desktop

Website is at the core of every business and naturally, customers of financial products want to be able to sign up for new accounts and products using their web browsers - whether on computers or via their mobile devices. Digital customer onboarding via Web Browsers is typically the most comprehensive and feature rich onboarding process. Customers are able to provide all their information, upload documents easily and complete verification process.

Benefits of digital self-onboarding for financial institutions

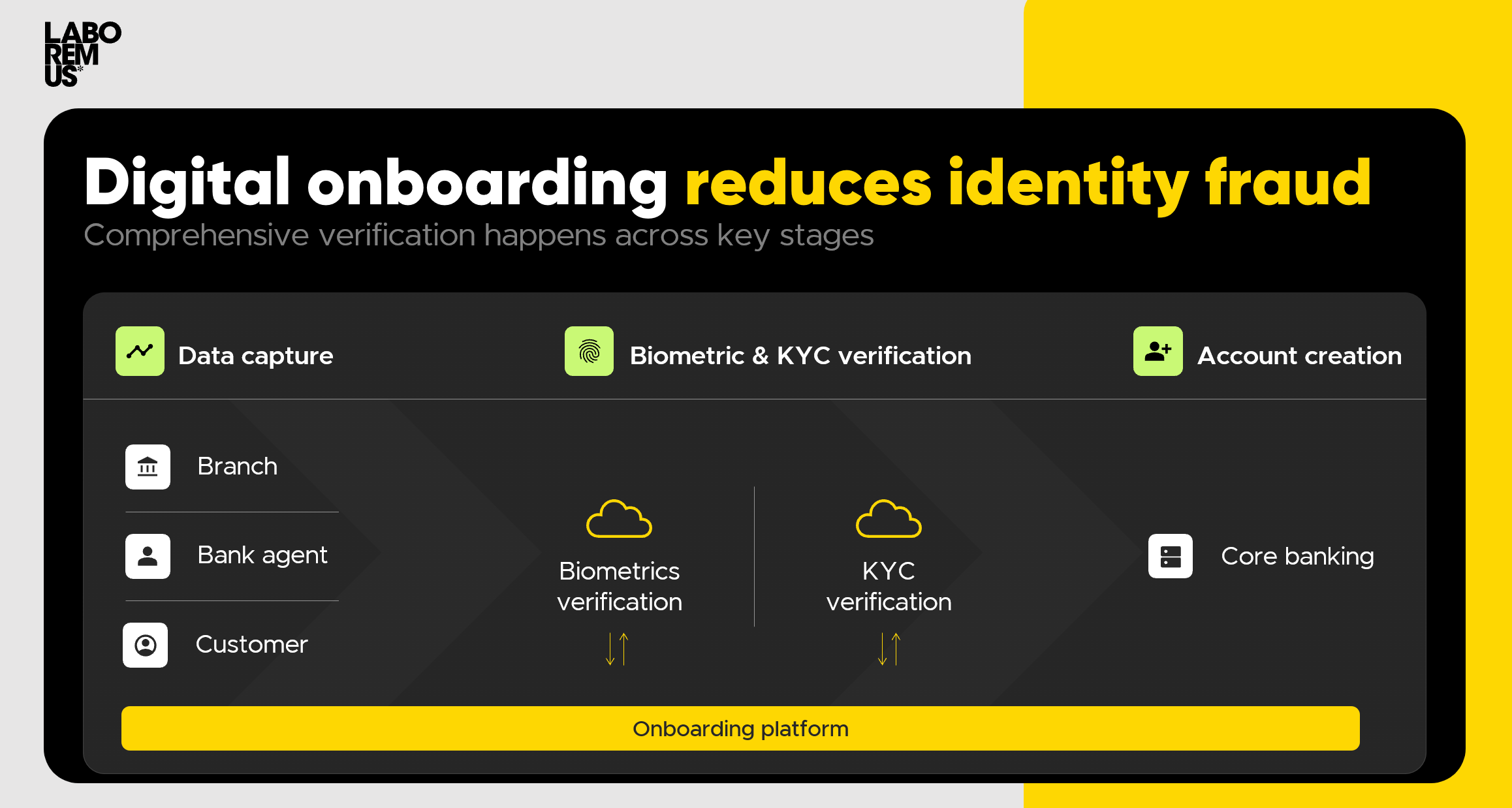

To effectively control and manage the risk from identity fraud your organisation’s customer onboarding process should be able to reliably verify that people are who they say they are. This prevents fraudsters from entering banking systems and creates a barrier on the first checkpoint.

A fully automated identity verification and onboarding process includes ensures that your customers enter the correct information during account opening, they upload appropriate identity documents and validate their personal details before submission.

The automated background checks then sync up with government databases to validate the entered information and ensure your onboarding process meets all regulatory standards.

Laboremus' digital self-onboarding process covers data capture, biometrics and KYC verification and syncing up seamlessly with your core banking system for account creation.

- Identity check

- KYC checks

- AML-PEP checks

- Data completeness and accuracy

- Risk profiling

The biggest advantages financial institutions experience with digital self-onboarding are:

Current manual processes for customer onboarding are high-friction in nature. Customers need to visit a physical location, carry all their documents, stand in queues, wait for their turn, deal with paperwork and often end up making mistakes while writing down their details.

Crucially the process is unnecessarily long. For a customer with manual onboarding it can often take multiple days and even weeks to get onboarded and start using their new account.

Digital onboarding removes these sources of friction from the account opening process. When properly designed and secured, a customer onboarding process with complete KYC can be completed in minutes.

Faster onboarding is a source of competitive advantage among financial institutions as it engages the customer in that moment when they desire to be a paying client, and delivers instant gratification in return.

B. Streamlined operations and wider market reachA well-designed digital onboarding process is simple to understand and implement.

Removing paperwork and moving to a data-driven digital customer acquisition helps financial institutions streamline their operations. The resources that were previously spending significant time helping customers fill up paperwork and on performing manual KYC checks can be reallocated to better serving customers.

A digital onboarding solution, boosts the reach of the bank by allowing customers from remote parts of the country the ability to open new bank account even if they are thousands of miles away from the nearest physical branch.

Digital onboarding also offers a multilingual user interface. This means that businesses can use digital onboarding solutions to verify people in their native language from different backgrounds and nationalities.

Digital onboarding process crucially uses multiple data validation procedures to ensure that customer data is collected without errors and gaps. With better form workflows, autofill to prevent asking the same questions, real-time data validation, user-friendly and interactive interface, and digital signatures, financial institutions can use digital self-onboarding to always collect comprehensive and accurate customer data.

More importantly, digital onboarding starts an omni-channel banking experience across mobile, internet, and physical channels which banks and financial institutions can leverage as a focal point to offer a incredible user experience to their customers.

All user provided customer data is validated to ensure clean, accurate inputs and once added is automatically verified against centralised government databases.

Digital onboarding platforms are easy to customise to adhere to local regulatory requirements. There are various built-in security measures in digital onboarding to maintain strict security.

Real-time security precautions are also taken; the biometric pattern of the face certifies the accurate online identification and life existence of the individual. Such security features lead to the prevention of identity theft and enhanced data security.

Digital self-onboarding when implemented correctly with the right technology reduces the risk of identity theft and account fraud significantly. This is because identity verification technology can check identity documents against other data sources like government ID database. This makes it much harder for someone to use a fake identity to open an account.

Digital onboarding in banking also helps to comply with anti-money laundering (AML) regulations. This is because once customer identity if verified, it is then screened against the AML watch lists to determine whether the customer can access financial products. This helps to prevent criminals from using your bank to launder money.

How digital self-onboarding reduces the risk of identity fraud

Digital self-onboarding when implemented correctly with the right technology reduces the risk of identity theft and account fraud significantly.

The most effective place to stop fraud is at the starting point of your organisation’s relationship with your customer: during the onboarding process. It’s the most crucial touchpoint for protecting the business from fraud and for establishing a stellar customer experience.

Modern identity verification solutions can check identity documents against other data sources like a government ID database. This makes it much harder for someone to use a fake identity to open an account.

Digital onboarding in banking also helps to comply with anti-money laundering (AML) regulations. The verified identity is also screened against the AML watch lists to determine whether the customer can access financial products. This helps to prevent criminals from using your bank to launder money.

STREAMLINE by Laboremus adds the crucial layer digital customer onboarding with identity verification within your existing digital technology framework. From data capture, to customer due diligence and account creation.

With this crucial step, anytime data is captured by your online banking channels, it goes through a comprehensive system of KYC, Biometrics and AML/PEP checks. Only once that data passes all the checks can the information be committed to your core banking system.

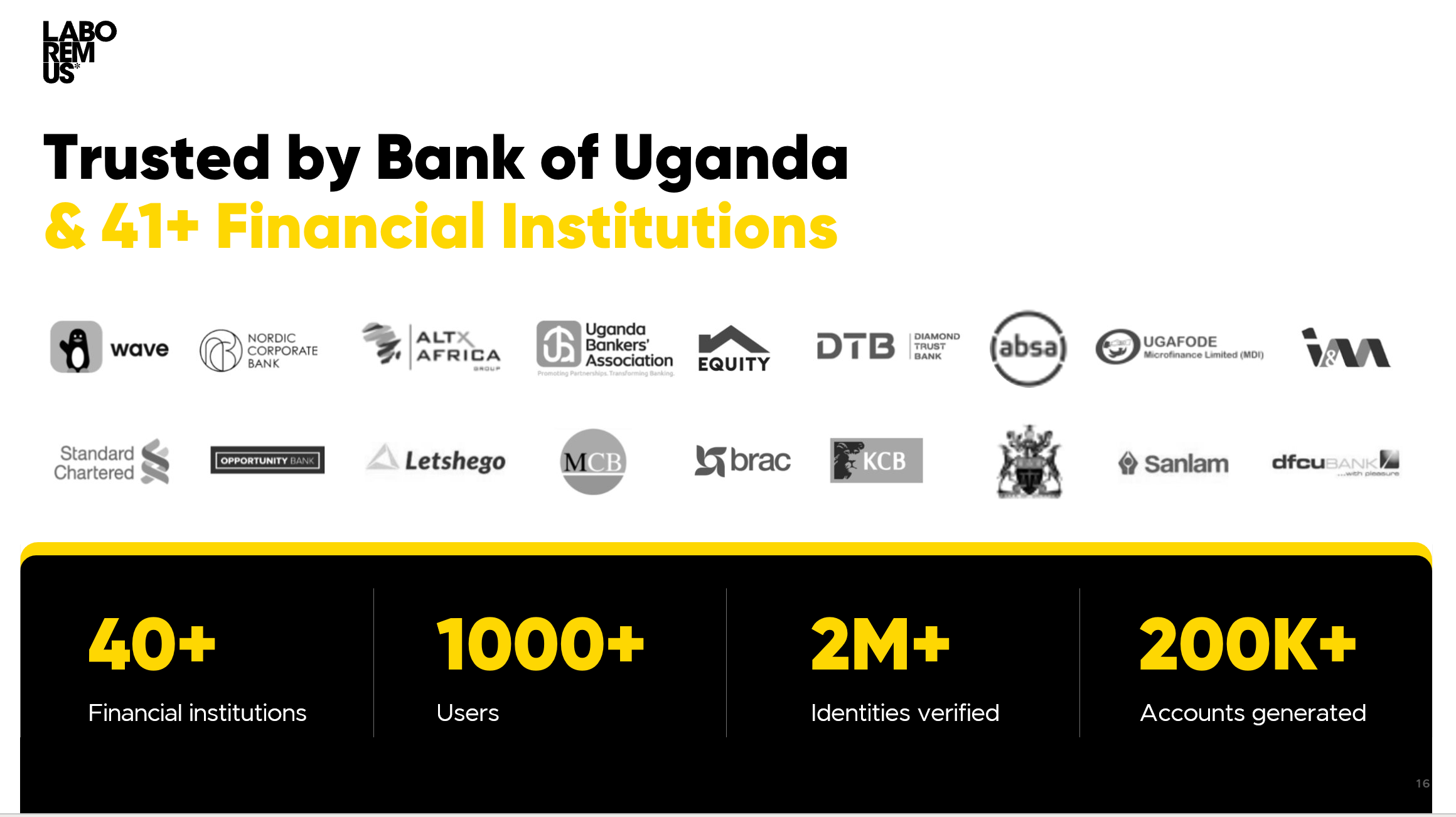

Laboremus is leading the change towards digital banking in Africa

STREAMLINE by Laboremus helps you acquire customers faster with reliable KYC / KYB and digital customer onboarding. Onboard customers in minutes by automating KYC checks and digitally establishing customer identity.

Partnerships with Government Orgs makes Laboremus the most reliable identity verification and onboarding platform in Africa.

For more information on STREAMLINE by Laboremus and our digital KYC, KYB and customer onboarding solutions, please visit www.laboremus.ug. You can also connect with one of our product experts to understand how you can automate customer due diligence and onboarding for your organisation.