Politically exposed persons (PEPs) pose a higher risk of corruption and involvement in money laundering and/or terrorist financing. This risk is significantly higher in Africa. To mitigate the potential risks posed by such activities, financial regulators require financial institutions (FIs) to implement enhanced due diligence (EDD) measures and clearly identify PEPs. These measures include verifying additional customer identification documents and establishing the source of funds or wealth for each entity or individual.

To achieve this financial institutions need accurate and up-to-date PEP data, readily accessible across their banking infrastructure. Using this data validation they can reliably screen entities during onboarding to ensure a comprehensive risk assessment on that specific customer. The monitoring continues during the customer lifecycle for periodic monitoring.

The accuracy and reliability of the data used to screen a PEP is important. High-quality data ensures relevant PEP profiles are identified accurately, minimising false positives and negatives. Poor data can lead to missed or misidentified PEPs, undermining the effectiveness of the screening process and exposing financial institutions to regulatory non-compliance and reputational risks.

In this article, we summarise key considerations for financial institutions and banks to build a reliable PEP due diligence process. We also detail how STREAMLINE by Laboremus achieves this using up to date and highly reliable PEP identification.

Guiding principles to build a reliable PEP screening process

A reliable PEP screening process relies on a few key elements for success:

- Quality of data: Customer data is critical for designing a reliable PEP process. It directly translates into the ability to quickly and accurately determine PEP status.

- Interfacing with global databases: Comprehensive PEP screening process includes screening customers against multiple databases across international, regional, local, and proprietary sources.

- Risk modelling: Customisable search profiles should be used to apply different search settings to groups of customers based on a firm’s business model and risk appetite.

- Ongoing monitoring: As PEP legislation evolves over time, businesses must proactively monitor regulatory trends to understand their implications and adapt their processes accordingly, ensuring ongoing adaptability and compliance.

By embracing these guiding principles and key considerations, FIs can establish a robust and efficient PEP screening process, bolstering their ability to combat financial risks and safeguard their operations with confidence.

General categorisation of PEPs by regulators

Regulators define PEP as an individual who is or has been entrusted with a prominent public function. Due to their position and influence, it is recognised that many PEPs are in positions that can be abused for the purpose of committing money laundering and related crimes.

There are three main categories of PEPs:

- Foreign PEPs: Individuals who are or have been entrusted with prominent public functions by a foreign country, for example:

- Heads of State or of government.

- Senior politicians.

- Senior government.

- Judicial or military officials.

- Senior executives of state-owned corporations.

- Important political party officials.

- Domestic PEPs: Individuals who are or have been entrusted domestically with prominent public functions, such as those listed above.

- International organisation PEPs: Persons who are or have been trusted in the past with a prominent function by an international organisation. This may refer to members of senior management or individuals who have been entrusted with equivalent functions, i.e., directors, deputy directors, and members of the board or equivalent functions.

PEP identification levels in STREAMLINE by Laboremus

One of the key challenges PEP data providers face is the lack of a universal definition of a PEP.

This is why STREAMLINE by Laboremus manages PEP identification in a way that aligns with the needs of financial institutions in Africa.

At the top level there are 4 classes:

- National

- International

- Regional

- Local

Each PEP class contains several taxonomies that are purposely granular, enabling analysts to select the relevant PEP categories for countries with varying levels of robust regulations.

Level 1 PEP: National

The first PEP class contains all taxonomies with national-level PEPs such as:

- National legislatures

- National cabinets

- Central banks

- Armed forces, police, fire service, and intelligence agencies

Level 2 PEP: International

The second PEP class includes:

- Members of regional governments, parliaments, and judiciary.

- Senior officials and functionaries of international and supranational organizations and diplomatic missions.

Level 3 PEP: Regional

The third PEP class related to:

- National level state-owned enterprises.

- Public sector institutions under regional level administration (eg regional agency, regional state-owned enterprises).

Level 4 PEP: Local

And the fourth PEP class contains:

- Mayors and members of local, county, city, and district assemblies.

- Senior executives of local governmental bodies (agencies, state-owned businesses)

- Judges of local courts.

Advantages of STREAMLINE by Laboremus in PEP filtering

More accurate

The taxonomy is designed to help users reduce false positives and negatives by narrowing down the screening to a particular category.

Wider reach

With Laboremus can screen new customers against international lists for PEPs which improves the accuracy and makes it more likely that PEPs are correctly identified regardless of to which countries their influence extends or not.

Reliably consistent

The unique value added consists in attributing a standardised set of definitions to a range of political and governance systems, which help the analyst assess their clients’ risk vis-a-vis the relative level of power they hold.

Designed for Africa

The system was built in Uganda and keeps a strong focus on the unique challenges of banks and financial institutions in Africa. STREAMLINE by Laboremus thus ensures higher accuracy and better compliance for financial institutions that operate in African countries.

Laboremus is leading the change towards digital banking in Africa

STREAMLINE by Laboremus helps you acquire customers faster with reliable KYC / KYB and digital customer onboarding. Onboard customers in minutes by automating KYC checks and digitally establishing customer identity and running deep customer due diligence.

Laboremus is creating a safe, reliable digital infrastructure for financial inclusion in Africa

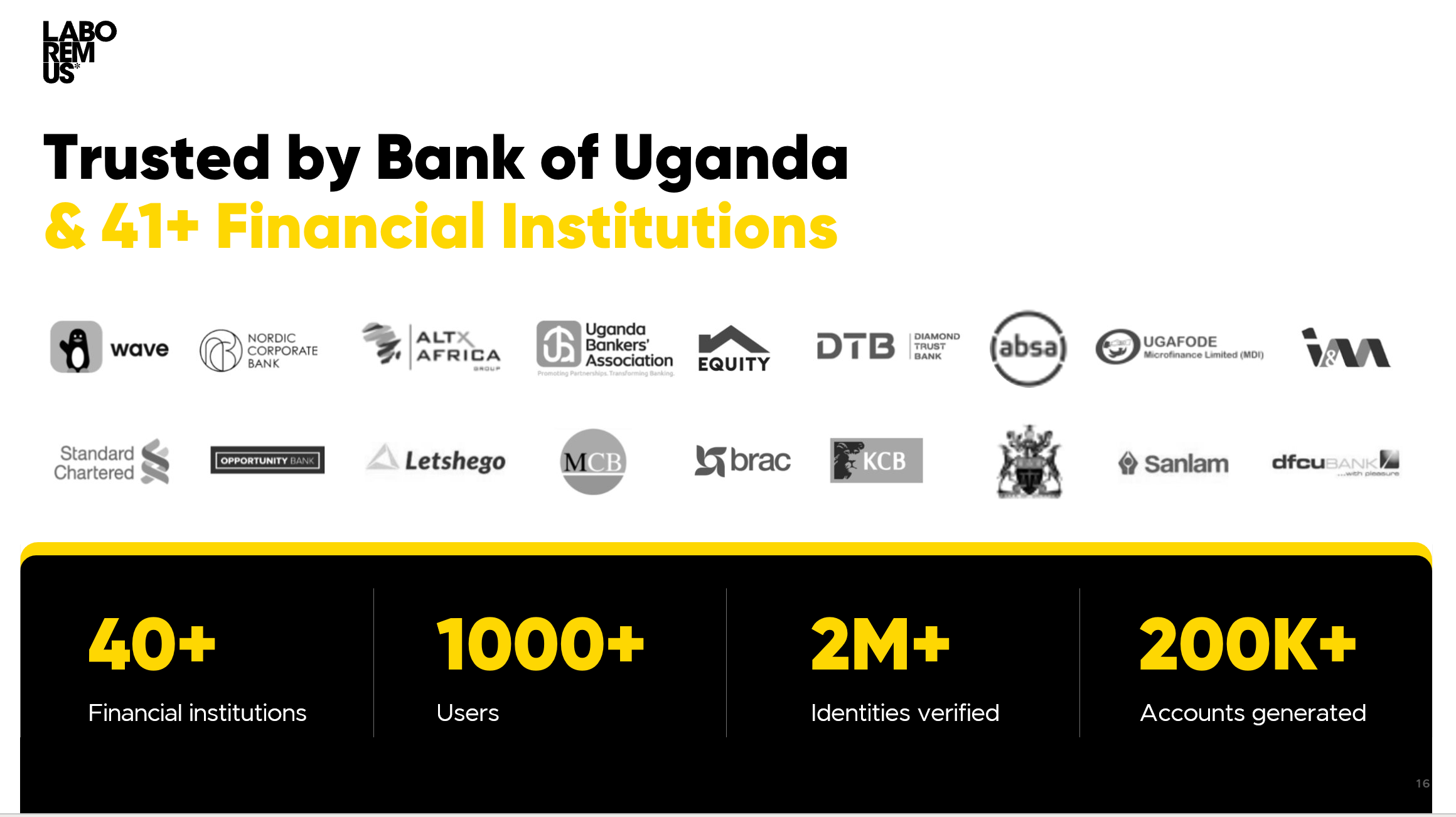

Partnerships with Government Organisations makes Laboremus the most reliable identity verification and onboarding platform in Africa. STREAMLINE by Laboremus powered AML/PEP verification is used by leading banks in Africa.

In Uganda, Laboremus is used by over 40 financial institutions and is trusted by Bank of Uganda and Uganda Bankers Association.

For more information on STREAMLINE by Laboremus and our digital KYC, KYB and customer onboarding solutions, please visit www.laboremus.ug. You can also connect with one of our product experts to understand how you can automate customer due diligence and onboarding for your organisation.